SMSFs are sexy. But is it right for you? Here is everything you need to know

There is $2.6 trillion in superannuation assets and about 30 per cent of that ($727 billion) is held in self-managed superannuation (SMSF) funds, with more than 60,000 Australians setting up a SMSF each year. SMSFs are not only complex and time consuming to manage but are extensively regulated. Understandably, SMSFs are not for everyone. So here are some tips to keep your retirement nest egg in check to also help you determine if a SMSF is for you.

Have your super all in one place

There is $17.5 billion in lost and unclaimed super across Australia. If you don’t know where your super is and don’t have all your super in one place, you could not only be paying for excess insurance and fees, but some life insurance policies could be voided and not pay out if an alternate policy is claimed.

You can track down your lost super, via the Australian Taxation Office’s myGov website and then roll it into your SMSF. Or, if you have an adviser, they can do this for you.

Costs

It’s important that you consider the annual running costs of a SMSF, as that can have an enormous impact on investment returns and the size of a superannuation account over time.

Consider how much your SMSF is costing you, from establishment costs, ordering the trust deed, to administration costs, annual audits, to the ATO supervisory levy and taxation lodgment. If you want a corporate trustee, i.e. a shelf company to be the trustee, then you will need to add an extra to the startup costs. Plus, you also need to consider the advice costs if you receive general or personal advice.

Are you taking advantage of existing contribution caps?

It’s important that you consider the annual running costs of a SMSF, as that can have an enormous impact on investment returns and the size of a superannuation account over time.

Consider how much your SMSF is costing you, from establishment costs, ordering the trust deed, to administration costs, annual audits, to the ATO supervisory levy and taxation lodgment. If you want a corporate trustee, i.e. a shelf company to be the trustee, then you will need to add an extra to the startup costs. Plus, you also need to consider the advice costs if you receive general or personal advice.

Salary sacrifice and personal contributions

Salary sacrifice is an agreement between you and your employer where your employer pays part of your pre-tax salary into your superannuation. Salary sacrifice allows that portion of income to be taxed at a maximum of 15 per cent, rather than your marginal tax rate (which may be up to 45 cents in the dollar (45 per cent).

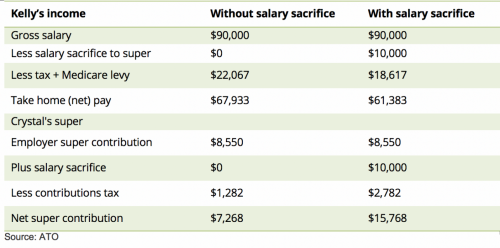

Personal contributions, such a salary sacrifice, are claimed as a deduction when you submit your tax return, reducing your assessable income. For example, if Kelly Dwyer earns $90,000 before tax, excluding her employer’s super contribution and she decides to redirect $10,000 of her pay into salary sacrifice super contributions, she will save $3,450 in tax, with the extra money going into her super fund.

Example of Kelly’s salary sacrificing

Kelly earns $90,000 pre-tax, excluding the superannuation guarantee. If she redirects $10,000 of her pay into salary sacrifice super contributions, she will save $3,450 in tax, with the extra money channeled into her super fund.

The figures are estimates only and are based on 2018-19 income tax rates, including the low-and middle-income tax offset, and a Medicare Levy of 2%. Employer superannuation guarantee contributions remain the same after salary sacrifice.

In the scenario, Kelly’s take-home pay drops by $6,550, but she saves $1,950 in tax on income and super and she will have an extra $8,500 in her superannuation.

Concessional contributions (before tax)

Concessional contributions are contributions made into your superannuation account each financial year. Contributions include salary sacrifice contributions and superannuation payments from your employer (superannuation guarantee payments). These contributions are taxed inside super at the concessional rate of 15 per cent. Concessional contributions are subject to a yearly cap, and according to the ATO:

- From 1 July 2018, members can make ‘carry-forward’ concessional super contributions if they have a total superannuation balance of less than $500,000. Members can access their unused concessional contributions caps on a rolling basis for five years. Amounts carried forward that have not been used after five years will expire.

- The first year in which you can access unused concessional contributions is the 2019–20 financial year.

Non-concessional contributions (after-tax)

Non-concessional contributions are contributions made into your super fund and are not included in your super fund’s assessable income, as they have generally already been taxed. A tax deduction cannot be claimed on these contributions.

It is also important to note that if you exceed your concessional contribution cap, excess contributions are then classed as non-concessional contributions for that respective financial year. Can we discuss what the caps are i.e. $100K p.a. and the bring forward rule?

Government Incentives

It’s also important that you and or your spouse are taking advantage of the government incentives where possible

- The government co-contribution: If you earn less than $52,697 before tax, you can earn up to $0.50 for every $1 contributed into super and the government will give you up to $500 in co-contribution into your super

- Spouse contribution: If your partner/spouse earns less than $37,000 you can claim an 18 per cent tax offset on up to $3,000 that you contribute into his/her super. Then you can access the maximum tax offset of $540 on your assessable income.

What else you need to know

- Non-concessional contributions are subject to a yearly cap with potential bring forward rules available.

- If a person’s non-concessional contributions exceed the cap, a tax of 47 per cent is levied on the excess contributions.

- From 1 July 2017, the non-concessional contributions cap is $100,000 for members 65 or over but under 75.

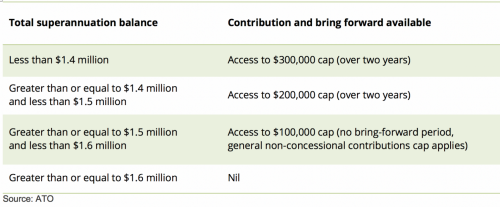

- Members under 65 years of age have the option of contributing up to $300,000 over a three-year period, depending on their superannuation balance.

Contribution and bring forward rules for under 65’s is outlined below.

Insurance

As your life changes, so should your insurance. You may not need as much insurance if you have paid off your mortgage, or if your children are no longer dependents. Whatever the case may be, you shouldn’t have too little or too much insurance, as you don’t want to be over insured and paying for insurance that you and or your family don’t need, but you also need to ensure that you are not underinsured as well.

You should make sure that if something unforeseen was to happen, you have adequate cover and peace of mind. Equally so, you need to ensure you are also getting the best deal. Are your premiums competitive. All these factors need to be taken into consideration for your SMSF.

A financial adviser or planner can help you compare products, find cheaper premiums and find out if you are insured for the correct amount and have the correct terms.

Paperwork, admin and compliance

Trustees are required to keep records for a minimum of five years for compliance and auditing purposes.

You might like to

- Manage everything yourself

- Or have an adviser/financial planner that does it for you

- Or outsource your administration and compliance management,

There are now various providers competing for your business to manage your SMSF admin, paperwork, and compliance. These providers will keep transaction records, operating statements, copies of all SMSF annual reports lodged and other statements required for the ATO for your SMSF.

Other necessary documents that need to be kept for a minimum of 10 years include; minutes of trustee’s meetings and decisions, trustee declarations recognizing their obligations and responsibilities, etc.

Trustee

There are two different types of ways you can set up a SMSF, either with individual trustees, where up to four people can be trustees of the fund, or you can have a corporate trustee, where a company acts as trustee of the fund. Whichever you chose, there are impacts on costings and responsibilities.

Investing your SMSF

One of the reasons you may be considering a SMSF is to get access to other assets that you couldn’t ordinarily get access to with a retail or industry superannuation fund, for instance, you may want to invest in direct (physical) property or direct shares. SMSFs are able to hold a very wide range of assets ranging from hedge funds, to commodities, to currencies, artwork, collectables and many other assets that require specialist investment advice

Estate Planning and Binding Death Nominations

When a SMSF member dies, the SMSF will generally pay a lump sum or income stream to a dependent or beneficiary of the deceased. If the trustees or member(s) have not set up a binding death nomination, then the SMSF trustees may exercise their discretion to determine who should receive the super benefits, subject to the provisions of the SMSF trust deed. Generally, the death benefit will be paid to an dependent if there is no binding death nomination form

Tax file number (TFN)

And lastly you should make sure your SMSF has your and your members TFNs, otherwise, concessional (before-tax) contributions will be hit with additional tax, and non-concessional (after-tax) contributions will not be able to be made.

Published: 1 April 2019

By Jessica Amir and Katrina Bullock