Launch Series 63

Dynamic Multi-Asset Momentum Index

The various features of the Index include:

Diversification

The Index allows investors to get a diversified exposure across 3 asset classes and 3 different geographical regions. This reduces the risk that the Index is overly exposed to a specific market.

The index allocates into futures contracts across:

- 3 Asset Classes: Fixed Income, Equities and Commodities; and

- 3 Regions: US, Europe, and Japan;

There are 12 component indices in total that the Index can potentially invest into:

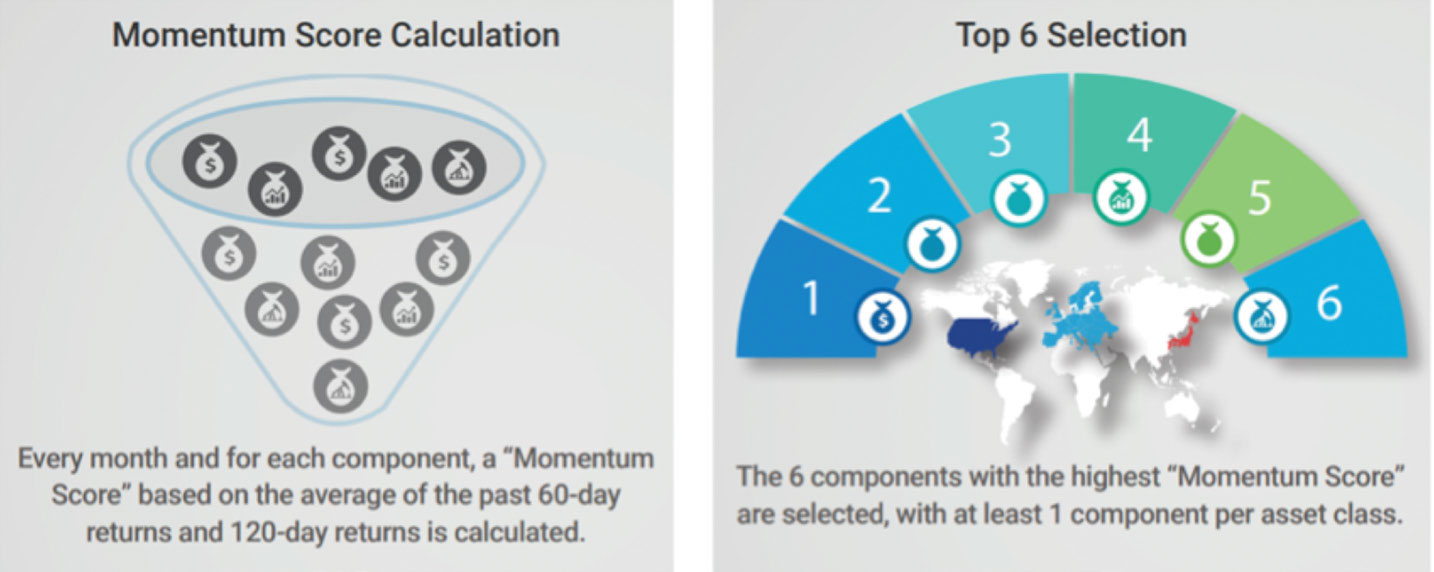

Momentum and Monthly rebalancing

The Index seeks to derive returns from assets with a positive price trend. The performance of the Index is driven by the 6 components that have the best recent performance within the universe rebalanced on a monthly basis. Recent performance is measured by the average of the previous 60-Business Days performance and the previous 120-Business Days performance, provided that at least 1 component index per asset class is selected.

Risk Management

The Index uses a 2-step risk management mechanism:

- Firstly, on a monthly basis, the portfolio risk is divided equally across the 6 best performers. It uses a technique called Equal Risk Contribution (ERC), which targets a portfolio with a maximum volatility of 5% and a maximum leverage of 200%. The ERC principle is that each component has the same contribution to the portfolio risk;

- Secondly, on a daily basis, as an additional protection and in order to limit negative performance in extreme market conditions, a risk control mechanism is used. It ensures that the volatility will remain close to the 5% target by temporarily reducing the exposure in situations where the volatility of the ERC portfolio exceeds 6%.

A summary of the key features are as follows:

Key risks:

Please review the key risks on page 10 of the PDS as well as the Target Market Determination (TMD) before investing.

Offer Open

Request the PDS and TMD