What is Inflation and what risk does it pose for investors

by Alexander Edmonds – Investment Manager

The world’s biggest peace time stimulus response and the rollout of vaccines globally could have a significant effect on the speed of the global economic recovery. Monetary and fiscal policymakers worldwide, in particular the U.S, are focused on policies that stimulate economic growth. Central banks will also look to prevent inflationary pressures becoming too high and unsustainable posing a significant threat to investors portfolios and savings.

What is inflation and how does it impact me?

Inflation is the sustained rise in price for goods and services. There are several theories and debates as to how exactly inflation occurs and the two main schools of thought regarding inflation are Keynesian Economic Theory and Monetarism. Keynesian Economic theory puts an emphasis on aggregate demand for goods and services and sees this as the primary driver of inflation. Monetarism focuses on the overall supply and velocity (circulation) of money- if there is more money chasing the same number of goods then this could influence what people are willing to buy goods for, again potentially creating upwards pressure on pricing.

Recently, we have seen unprecedented fiscal responses by governments all over the world as a response to COVID. Although no one is questioning whether this response was necessary or not, its no wonder people are starting to get concerned that the increase in the total supply of money could cause rapid price inflation. This is also exacerbated by record low interest rates, disincentivizing people to keep money in their bank accounts (which makes spending it all that easier- money velocity).

The reason that this poses a threat to both consumers and investors is that the value of both dollars and the return on assets is reduced if inflation is high. For example, if the rate of inflation sits at 2% and the return that an investor gets on their investment is 5% per annum, the real rate of return on the investment is 3% as the value of the dollars produced by that return are actually worth less than when the investment was made.

Why haven’t I needed to be concerned about inflation in the past?

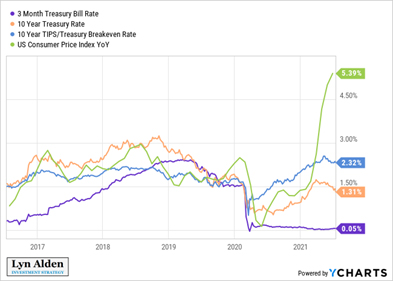

Inflation has been very low for a considerable time. Core inflation in Australia has been under the RBA’s 2-3% policy target range since Q4 2015 and has not been above the range since early 2010 during the mining boom. There have been a number of factors that have kept inflation low, however the main influence has been the increased adaption and acceleration of technology.

Technological advancements reduce inflation by creating efficiencies in the creation process of goods and services. Eventually that saving should get passed down to the consumer through the price of the product as manufacturers are able to produce the product at a lower cost. This also puts downward pressure on wages (a key factor in inflation) as it enables workers to produce more output- theoretically keeping the costs of goods and services lower for longer.

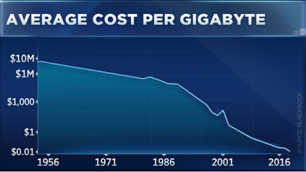

A great example would be the cost of computing power and data storage. The below graph from Blackrock shows the reduction in the cost of a Gigabyte from the 1950’s until now. Rick Reider of Blackrock suggests that today’s phones would be worth around $1.4million dollars based on the storage and computing costs in 1991.

Phones also perform other tasks such as being calculators, clocks, GPS devices and much more. This effectively creates competition in the markets for other goods, driving prices down for those other goods.

How do different assets perform in a high inflation environment?

Some investments perform better than others in higher inflation environments:

REITS and Infrastructure Assets:

Real assets such as Real Estate Investment trusts and Infrastructure can perform well during periods of higher inflation relative to the market. They typically have yields that are linked to the consumer price index or another measure of inflation. This serves to make sure that the rent received from holding real assets does not lose value in real dollar terms. Some infrastructure assets are considered essential in nature and are more robust against economic shocks and negative policy changes.

Some Infrastructure assets tend to be highly geared, therefore if interest rates rise due to an overheating economy, this could lead to a reduction in the value of highly geared infrastructure companies as an increase in the cost of debt financing can eat away at the yield generated from assets.

Good for Value stocks, bad for growth stocks:

Companies with high nominal pricing power have the ability to pass additional costs onto consumers without impacting demand significantly. If a company has the power to change their product and service offering in line with inflation (or even higher than inflation) then they should outperform the market. These are typically larger companies which have a substantial following of devoted customers willing to pay the higher product prices, or companies that dominate a market that produce a product or service that is considered a necessity.

Higher interest rates (as a response to inflation) also influence the rate at which growth stocks are valued. As growth stocks are often valued based on their future earnings potential, a change in the interest rate changes the rate at which the future cash flows are discounted back to their present value. As such, higher interest rates have a higher proportionate negative effect on growth companies that don’t have strong current earnings.

Gold:

Historically people have considered Gold to be a hedge against inflation. If a countries currency is losing value, people will often purchase Gold in an attempt to maintain purchasing power. The argument for Gold as a hedge against inflation has recently lost steam as the correlation between inflation and Gold has reduced in the short term.

There is a strong inverse relationship between real interest rates and the value of Gold. When there is a sustained period of high inflation, central banks often will increase interest rates. Safe haven assets that don’t pay any yield don’t perform too well with higher interest rates as there is a greater opportunity cost of holding that asset vs having funds in an account or an asset earning yield. Therefore, Gold is a better indicator of perceived “Future Inflation” as real interest diminish prior to a central bank response, Gold typically moves higher.

Wrapping it up:

Although the jury still isn’t out on whether we are going to see a period of high inflation or not. Most experts are suggesting investors position for some inflation through a well-diversified portfolio but remember to not panic. High inflation does “eat away” at low interest-bearing cash so it’s important for investors to stay invested in assets that they are comfortable with in the long term.

Disclaimer: The information in this document is of a general nature and should not be relied upon as it as been prepared without taking into consideration the objectives, financial situation or needs of any particular person. As a result, before on this information, a person should consider its appropriateness, having regard to their objectives, financial situation and needs. Information from third parties is believed to be reliable, however it has not been independently verified. While the information in the document is given by Sequoia Asset Management in good fair it does not warrant that it is accurate, reliable, and free from errors or omissions. Neither Sequoia Asset management or employees accept any responsibility for errors in or omissions from the information.